Last summer, a Reddit post from a 25-year-old software engineer went viral for a simple reason: he proved that his AED 10,000 monthly salary in Dubai left him with almost exactly the same savings as his ₹60,000 salary in India. The numbers stunned thousands of readers who had always assumed that Dubai’s tax-free income meant automatic wealth.

What the post really exposed was a gap between what salaries look like on paper and what they actually buy in daily life. That gap is exactly what purchasing power parity measures, and it is exactly why you need more than a currency converter to evaluate a Dubai offer.

PPP Calculator India Vs Dubai calculates purchasing power of your salary in India to live a similar quality of life in Dubai (UAE).

Key Takeaways

- An AED 360,000 salary in Dubai has the same purchasing power as roughly ₹31.5 lakhs in India, not the ₹92.20 lakhs you would get through a simple currency conversion.

- Dubai’s zero income tax is its biggest financial advantage, but housing, schooling, and healthcare expenses consume a larger share of your paycheck than they would in most Indian cities.

- PPP captures price differences for everyday goods, but it does not reflect the value of employer benefits like housing allowances, annual flights home, and family insurance, which can shift the real equation dramatically.

- The “3x rule” used by experienced expats suggests that a Dubai offer should be roughly three times your Indian in-hand salary to meaningfully improve your financial position.

Quick Reference: India vs Dubai PPP Salary Equivalents

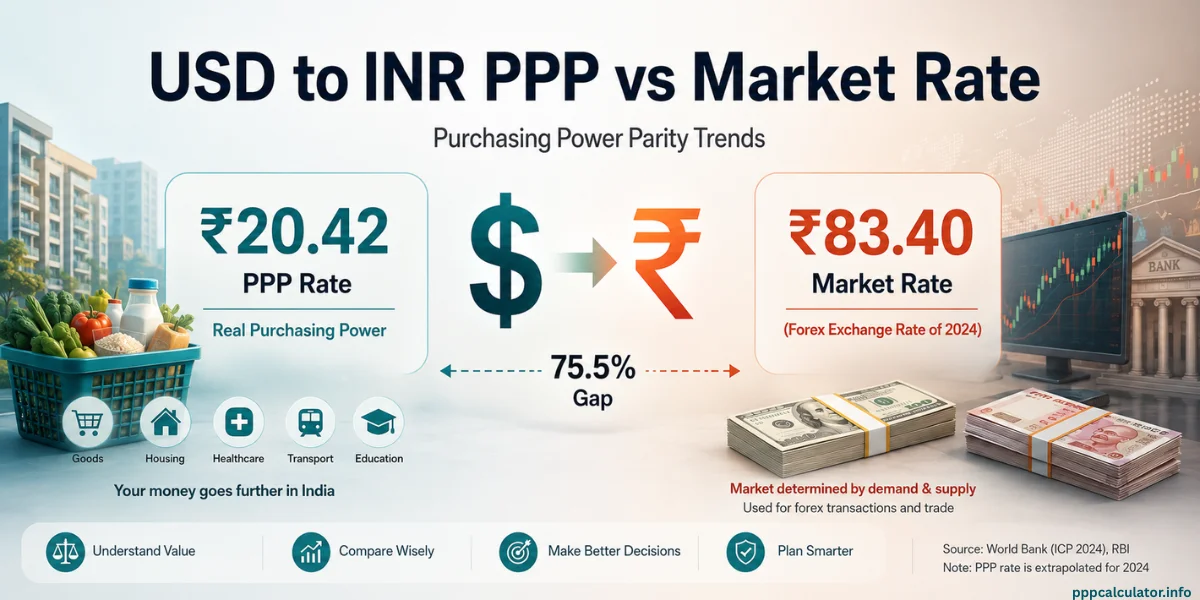

The table below shows what common Dubai salaries are worth in Indian purchasing power terms. These figures use World Bank PPP conversion factors (20.421988, UAE: 2.330334) and reflect equivalent purchasing power, not currency exchange.

| Dubai Salary (AED/year) | Dubai Salary (AED/month) | PPP Equivalent in India (₹/year) | PPP Equivalent in India (₹/month) |

|---|---|---|---|

| AED 180,000 | AED 15,000 | ₹15.8 lakhs | ₹1,31,500 |

| AED 360,000 | AED 30,000 | ₹31.5 lakhs | ₹2,62,900 |

| AED 600,000 | AED 50,000 | ₹52.6 lakhs | ₹4,38,200 |

How to read this table: An AED 360,000 annual salary in Dubai has the same purchasing power as earning approximately ₹30.7 lakhs per year in India. This means the goods and services you can afford with AED 360,000 in Dubai are roughly equal to what ₹30.7 lakhs buys in India.

For custom calculations with your exact salary, use our PPP calculator at home page or at the top of this page.

Why PPP Numbers Look So Different from Currency Conversion

If you convert AED 360,000 to Indian rupees using today’s exchange rate (roughly 1 AED = 25.51 INR), you get about ₹92 lakhs. The PPP equivalent is only ₹31.15 lakhs. That is a massive gap, and understanding why it exists is the key to making a smart decision about a Dubai move.

Exchange rates tell you how much one currency trades for another on financial markets. PPP tells you how much your money actually buys where you live. These are two completely different measurements. A haircut that costs AED 40 in Dubai might cost ₹200 in Bangalore. A plate of biryani that costs AED 25 in Karama costs ₹150 in Hyderabad. Multiply these differences across thousands of goods and services, and you understand why ₹30.7 lakhs in India stretches as far as AED 360,000 in Dubai.

This does not mean you should ignore exchange rates entirely. If you plan to send money home to India, the exchange rate matters enormously because remittances convert at market rates, not PPP rates.

A Dubai salary’s real advantage often lies in this combination: you spend at Dubai’s higher prices but save and remit at the favorable AED-to-INR exchange rate. The PPP vs exchange rate distinction is one of the most important financial concepts for anyone evaluating international opportunities.

The Tax-Free Advantage: What Zero Income Tax Actually Means

Dubai’s most famous financial perk is its zero personal income tax. The UAE does not deduct any income tax from your salary, which means your gross pay equals your take-home pay. For Indian professionals accustomed to losing a significant portion of their earnings to taxes, this is transformative.

- Under India’s new tax regime for FY 2025-26, the tax burden is substantial for mid-to-high earners. Income up to ₹12.75 lakhs (including standard deduction for salaried employees) is effectively tax-free. But beyond that threshold, rates climb quickly. For someone earning ₹30 lakhs in India, the effective tax rate lands around 15-17% after accounting for the new regime’s slab structure. At ₹50 lakhs, you are paying closer to 25% in effective taxes, plus the 4% health and education cess on top.

- In Dubai, that entire tax amount stays in your pocket. On an AED 30,000 monthly salary (roughly ₹50 lakhs at PPP), you keep every dirham. This single factor can close or even reverse the PPP gap, depending on your income level.

- Here is where the math gets interesting. For an Indian salary of ₹15 lakhs, the tax saving from moving to Dubai is relatively modest because most of that income falls in low tax brackets anyway. But at ₹30 lakhs and above, the annual tax saving becomes ₹4-8 lakhs or more, which is significant enough to shift the entire cost-of-living equation.

- The UAE also does not tax capital gains, dividends, or investment returns. If you invest from Dubai, your portfolio grows without the drag of Indian capital gains taxes. One Reddit user captured this perfectly when he noted that for anyone with meaningful savings invested in global markets, the absence of capital gains tax alone can justify the relocation.

However, the zero-tax promise comes with a critical nuance for Indian citizens. Your tax residency status under Indian law determines whether your Dubai salary truly remains untaxed. To qualify as a Non-Resident Indian (NRI), you must stay outside India for at least 182 days in a financial year. If you fail to meet this requirement, India can tax your worldwide income, including your Dubai salary.

The India-UAE Double Taxation Avoidance Agreement (DTAA) provides relief if you hold a UAE Tax Residency Certificate, but the paperwork and compliance requirements are real obligations that many first-time expats overlook.

Where Dubai Gets Expensive

PPP provides an honest national-level comparison, but it smooths over the specific categories where Dubai costs can spike dramatically. Three expenses consistently surprise Indian professionals relocating to Dubai: housing, schooling, and the invisible costs of setting up a new life abroad.

Housing Eats the Biggest Share

Rent is the single largest monthly expense for any Dubai resident. A one-bedroom apartment in popular expat areas like Dubai Marina or JLT runs between AED 70,000 and AED 110,000 per year, which works out to AED 5,800 to AED 9,200 per month. In comparison, a similar apartment in Bangalore’s Whitefield or Pune’s Hinjewadi costs ₹15,000-30,000 monthly. Even after adjusting for purchasing power, the Dubai apartment consumes a far larger percentage of your monthly income.

Budget-conscious expats stretch their salaries by choosing areas like Al Nahda, Dubai Silicon Oasis, or living across the border in Sharjah, where a one-bedroom starts at AED 2,800-3,250 per month. The trade-off is a longer commute, but many Indian families find the savings worthwhile. Whether your employer includes a housing allowance in your compensation package can mean the difference between struggling and thriving in Dubai.

Schooling is a Second Rent

For families with children, school fees represent a second major financial commitment that PPP alone does not capture. Indian curriculum schools (CBSE and ICSE) in Dubai charge between AED 8,000 and AED 25,000 per child per year. These are popular with Indian expat families and deliver solid academics at relatively affordable rates.

British, American, or IB curriculum schools jump to AED 30,000-100,000 annually per child. A family with two children in a mid-range international school can easily spend AED 50,000-70,000 per year on education alone. In India, comparable private schooling costs a fraction of this amount, even at premium institutions in metro cities.

The Hidden Setup and Ongoing Costs

Beyond rent and school fees, Dubai layers on costs that do not have direct equivalents in India. Security deposits for apartments (typically 5% of annual rent), DEWA (utility) connection fees, furniture purchases for unfurnished apartments, and Emirates ID processing fees all add up during the first few months.

Health insurance is mandatory for all residents, and while employers must provide coverage for employees, extending that coverage to family members often comes at additional cost. The UAE’s 5% VAT applies to most goods and services. Although lower than consumption taxes in most countries, it adds a consistent markup to daily spending that did not exist before 2018.

The Real Decision Framework: When Dubai Makes Financial Sense

PPP gives you a baseline. Taxes shift the equation. But the real-world outcome depends on the specific offer on your table. Experienced Indian expats in online forums consistently point to a practical rule: -Dubai offer should be roughly three times your current Indian in-hand salary for the move to deliver meaningful financial improvement.

This 3x benchmark is not arbitrary. It accounts for the higher cost of living, the loss of family support systems (which reduce costs in India in ways no spreadsheet captures), and the emotional and logistical costs of relocation. At 2x, you will likely match your Indian lifestyle without saving much more. Below 2x, you risk downgrading your quality of life.

- The equation tilts in Dubai’s favor when your employer covers housing or provides a housing allowance, which effectively removes your largest single expense. It also tilts favorably when you are a higher earner, because the tax savings compound. A professional earning ₹50 lakhs in India pays roughly ₹10-12 lakhs in annual taxes. In Dubai, that money stays invested. Over a five-year stint, the compounded tax savings alone can build a substantial financial cushion.

- On the other hand, the equation tilts toward India when your salary offer lacks major benefits, when you have school-age children who would need premium education, or when your family support system in India significantly subsidizes your current living costs. Home-cooked meals from family, shared housing, affordable domestic help, and the comfort of familiar surroundings carry real economic value that never appears in PPP comparisons.

For a deeper look at how PPP-based salary comparisons work across multiple countries, check our salary comparison by country guide.

Beyond the PPP Calculator

Our purchasing power parity calculator gives you the most reliable starting point for comparing salaries between India and Dubai. But some of the most important factors in this decision sit outside any calculator’s reach.

Dubai’s work culture is intense. Many Indian professionals report longer working hours and higher performance pressure compared to Indian corporate environments, particularly in the private sector. The flat organizational structures that enable faster career growth also mean there is nowhere to hide.

Remote and hybrid work arrangements, which have become standard at many Indian tech companies, are less common in Dubai’s private sector, where physical presence is still the norm in many industries.

Career acceleration is one of Dubai’s genuine non-financial advantages. Professionals working in multinational environments gain exposure to regional and global markets across the Middle East, Africa, and South Asia. Several expats have noted that Dubai compresses career timelines, offering senior-level exposure in three to five years that might take eight to ten years in Indian corporate hierarchies.

Then there is the question nobody puts in a spreadsheet: proximity to family. Weekend flights to India are short (3-4 hours to most Indian cities), but “short” and “free” are different things. The emotional cost of missing festivals, family events, and the daily closeness of parents and extended family is something every Dubai-bound Indian professional weighs privately, even if the financial math clearly favors the move.

How to Use PPP for Your Dubai Decision

Start by running your specific salary through our PPP calculator to get the baseline purchasing power comparison. Then layer in three adjustments.

- First, add back the tax savings. Calculate what you pay in Indian income tax at your current salary level and add that amount to the PPP equivalent. This gives you a truer picture of disposable income.

- Second, subtract Dubai-specific costs that PPP averages out. If your employer does not cover housing, deduct your estimated rent. If you have children, deduct school fees. These two items alone can shift the PPP result by several lakhs.

- Third, factor in the remittance advantage. If you plan to save and send money to India, your Dubai dirhams convert at exchange rates, not PPP rates. This means your savings in AED translate to significantly more rupees than the PPP number suggests, because AED is “overvalued” relative to purchasing power. The amount you save in Dubai buys more in India than the PPP number implies.

This three-step adjustment turns a general PPP comparison into a personalized financial analysis. To understand the methodology behind these calculations, read our guide on what is purchasing power parity and how the PPP formula works.

PPP Calculator India vs Dubai – FAQ

Ans: An AED 15,000 monthly salary has the purchasing power equivalent of roughly ₹15.8 lakhs per year in India. For a single professional, this is manageable if you choose affordable housing areas like Al Nahda or Sharjah and keep lifestyle expenses in check.

Ans: Using the PPP formula, ₹25,00,000 = AED 2,85,300 per year, or about AED 23,800 per month. However, since you pay zero income tax in Dubai, the in-hand comparison is more favorable. Your ₹25 lakh salary in India after taxes yields roughly ₹20-21 lakhs in hand.

Ans: The combination of zero income tax, higher gross salaries (typically 30-50% above Indian equivalents for similar roles), and the favorable AED-to-INR exchange rate for remittances creates a savings multiplier that PPP alone does not capture. An expat saving AED 5,000 per month accumulates roughly ₹1.28 lakhs in India per month at current exchange rates, which is a savings rate many Indian professionals earning similar PPP-equivalent salaries cannot match domestically, where taxes and lower gross pay reduce the savings pool.

Ans: No. PPP measures price equivalence for comparable goods and services, not the quality of public systems like roads, safety, healthcare, or governance. Dubai scores high on infrastructure quality, public safety, and administrative efficiency. These are genuine lifestyle improvements that have economic value but are not reflected in PPP conversion factors.

Ans: Use exchange rates for actual money transfers. When you send AED to India, your bank converts at the market exchange rate (approximately 1 AED = 25-26 INR), not the PPP rate. PPP is the right tool for comparing what your salary buys locally in Dubai versus what a salary buys locally in India. Exchange rates are the right tool for calculating how much your saved dirhams become when they land in your Indian bank account.

More India PPP Comparisons

Considering other destinations beyond Dubai? Compare purchasing power across corridors:

- PPP Calculator India vs US: The largest corridor for Indian tech professionals

- PPP Calculator India vs Canada – Immigration pathways and PR benefits for Canada-bound professionals.

- PPP Calculator India vs Germany – Social security contributions, and city-level cost differences.

Jitender is the founder and lead developer of PPPCalculator.info. He created this free tool to bridge the gap between currency conversion and real purchasing power, helping professionals across 50+ countries make informed salary decisions. He regularly translates complex World Bank and OECD data into practical guides for remote workers and expats.