Quick Reference: PPP Salary Equivalents:

| Your Indian Salary | Equivalent Purchasing Power in Germany |

|---|---|

| ₹15 lakhs/year | ~€51,500/year |

| ₹25 lakhs/year | ~€85,800/year |

| ₹40 lakhs/year | ~€1,37,300/year |

| ₹60 lakhs/year | ~€2,05,900/year |

| Your German Salary | Equivalent Purchasing Power in India |

|---|---|

| €50,000/year | ~₹14.6 lakhs/year |

| €80,000/year | ~₹23.3 lakhs/year |

| €1,20,000/year | ~₹35.0 lakhs/year |

Calculated using World Bank PPP factors: India 20.421988, Germany 0.700862

Your recruiter in Frankfurt just sent over an offer: €65,000 a year. You’re currently earning ₹28 lakhs in Pune. The euro number looks bigger. It feels like progress. But look at the quick reference table above and you’ll see that ₹28 lakhs requires around €96,000 in Germany to match the same purchasing power. That €65,000 offer is a lifestyle reduction of roughly 35%, not an upgrade.

Most people making this comparison convert currencies and stop there. At today’s rate, €1 is about ₹90, so €65,000 looks like ₹58.5 lakhs. That comparison is meaningless. Germany costs far more to live in than India, and the exchange rate captures none of that. Purchasing power parity accounts for it.

India vs Germany PPP guide uses World Bank PPP data to show what your salary actually buys in each country, with real numbers at each income level.

Key Takeaways

Germany’s cost of living is roughly 250 to 300% higher than India’s, which means the PPP conversion ratio between the two countries is steep. To match the purchasing power of ₹25 lakhs in India, you need approximately €86,000 in Germany. Most German professional salaries fall well below that, which means the India-to-Germany move is almost always a purchasing power reduction in the short term.

The headline salary numbers are misleading in both directions. German gross salaries look large in euros but lose 35 to 45% to taxes and social contributions before you see them. Indian salaries look modest in rupees but retain 76 to 80% as take-home and go further because costs are lower.

Germany’s total compensation includes mandatory unemployment insurance, pension contributions, and parental leave that do not show up in the salary number but have real monetary value, particularly for professionals in their 30s thinking about family or job security.

The EU Blue Card requires a minimum €48,300 gross salary for most roles, dropping to €43,760 for IT and STEM shortage occupations. Almost all professional offers qualify, so visa eligibility is rarely the constraint.

What PPP Actually Measures

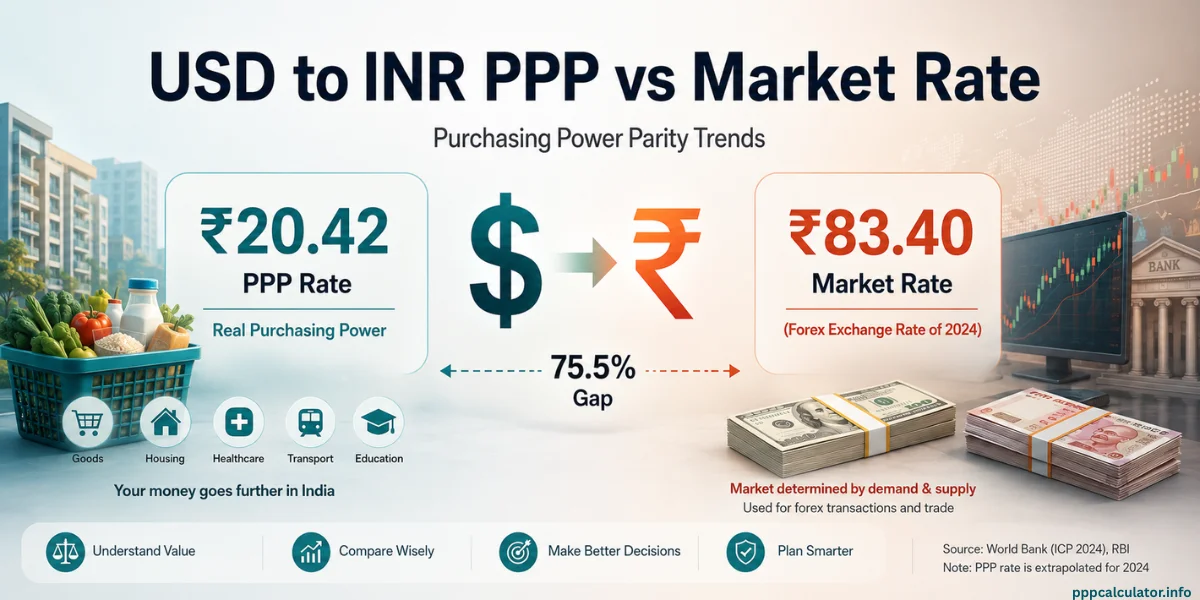

Purchasing power parity is not a currency conversion. It answers a different question: how much money do you need in Country B to live the same way you live in Country A?

The World Bank calculates this by comparing price levels across countries using a common basket of goods and services, rent, groceries, transport, healthcare, and so on. The result is a conversion factor. India’s 2024 factor is 20.421988. Germany’s is 0.700862. When you divide Germany’s factor by India’s, you get how many rupees of Indian purchasing power one euro of German purchasing power represents. The formula is:

Equivalent Salary = Your Salary × (Target Country PPP Factor ÷ Source Country PPP Factor)

So ₹25,00,000 × (0.700862 ÷ 20.421988) = approximately €85,800. That is what your Bangalore lifestyle costs in Berlin.

The ratio is asymmetric because the two economies price goods very differently. India is cheap relative to its income levels. Germany is expensive. The PPP formula captures that gap.

India vs Germany: The Numbers Side by Side

| Factor | India | Germany |

|---|---|---|

| Average IT Salary (Mid-Level) | ₹12-25 lakhs/year | €60,000-80,000/year |

| Cost of Living Index | 100 (baseline) | 250-300 |

| Rent (1BR City Center) | ₹25,000-40,000/month | €900-1,400/month |

| Income Tax Rate (Mid-Level) | 20-30% | 35-42% |

| Healthcare Cost (Annual) | ₹15,000-50,000 (private) | ~15% of salary (covered) |

| Public Transport (Monthly) | ₹800-1,500 | €80-100 |

| Restaurant Meal (Basic) | ₹200-400 | €12-18 |

| Groceries (Monthly, Single) | ₹6,000-10,000 | €250-350 |

| Work Week Hours | 45-50 hours (typical) | 40 hours (standard) |

| Paid Vacation Days | 12-20 days | 25-30 days |

Note: Indian figures represent major metro cities (Mumbai, Bangalore, Delhi). German figures represent major cities (Berlin, Munich, Frankfurt). Actual costs vary by specific location.

A restaurant meal in Berlin costs €15. In Mumbai it’s ₹300. A monthly transport pass is €90 in a German city versus ₹1,500 in an Indian metro. Multiply those gaps across rent, groceries, utilities, and insurance and you land at roughly three times the cost of living. German salaries compensate for that to some extent, but after PPP conversion the gap narrows significantly and often reverses.

Real Salary Examples: India to Germany

Let’s look at verified scenarios that show how PPP works in practice between these countries.

A software engineer earning ₹25 lakhs in Bangalore needs approximately €86,000 in Germany to maintain the same purchasing power. A Berlin offer of €55,000 or €65,000 is a step down in lifestyle terms, even before accounting for higher taxes. To genuinely improve on ₹25 lakhs, the German offer needs to clear €86,000.

A product manager at ₹40 lakhs needs roughly €1,37,000 to match that lifestyle in Munich. That figure is above what most mid-level German roles pay. The move is a purchasing power reduction unless the role comes with senior European compensation.

A data scientist at ₹30 lakhs needs about €1,03,000 equivalent in Frankfurt. Most German data science roles fall between €60,000 and €80,000, which represents a meaningful purchasing power gap. The career credentials and EU work experience can justify taking that gap, but it’s a trade-off, not an upgrade.

This is not an argument against moving to Germany. It’s the honest calculation that most comparison sites bury or get wrong by presenting euro salaries as automatic improvements over rupee salaries.

Real Salary Examples: Germany to India

For professionals returning from Germany, the PPP numbers work in the other direction and often surprise people.

An engineering manager earning €80,000 in Berlin has Indian purchasing power equivalent to about ₹23.3 lakhs. An Indian company paying ₹55 to 70 lakhs for the same role is offering two to three times more purchasing power than the German salary. People who have spent years associating euros with financial security find this counterintuitive, but the math is straightforward.

A marketing director earning €70,000 in Hamburg has Indian purchasing power of about ₹20.4 lakhs. A Delhi or Bengaluru offer at ₹45 lakhs puts you comfortably ahead.

A UX designer earning €50,000 in Cologne has Indian purchasing power of roughly ₹14.6 lakhs. Indian design roles at ₹20 to 25 lakhs in Bangalore or Mumbai are financially stronger on a PPP basis.

The pattern is consistent across roles. Germany is an expensive country. Once you account for that through PPP, competitive Indian salaries regularly outperform European equivalents in real purchasing power. The trade-offs are the healthcare system, the work culture, the career exposure, and the personal reasons that make people choose to live in Europe regardless of what the numbers say.

What Your Money Actually Buys: Cost Categories

Understanding specific expense categories helps contextualize PPP calculations and salary decisions.

Housing is where the difference hits hardest. A one-bedroom apartment in central Bangalore runs ₹25,000 to 40,000 a month. The same apartment in Berlin is €900 to 1,400, which at today’s rate is ₹81,000 to ₹1,26,000. Munich and Frankfurt are higher still, with one-bedrooms regularly exceeding €1,500.

Cities like Pune or Hyderabad offer comparable quality housing for ₹20,000 to 35,000. Germany also requires three months rent as a security deposit upfront plus the first month in advance, so you need ₹3 to 5 lakhs just to sign a lease before accounting for any other setup costs.

Groceries in Germany run two to three times higher than India. Basic items cost more across the board. The quality standards are different, particularly for fresh produce, but the rupee-equivalent grocery bill in Berlin is substantially higher than in any Indian city.

Indian restaurants in Germany, if you’re looking for home-style food, cost far more than eating local German food. Budget ₹80,000 to ₹1,10,000 per month equivalent for food in a German city versus ₹10,000 to 20,000 in an Indian metro.

Transport in Germany is good but expensive relative to India. Monthly passes run €80 to 100. Most German city professionals do not need a car because public transport is comprehensive. India’s metro systems charge ₹800 to 1,500 monthly for comparable coverage, though many Indian cities require a car for practical reasons, which adds its own cost.

Healthcare differs structurally. German health insurance is mandatory at roughly 15% of gross salary, split with your employer. You pay about 7.5% and your employer pays the rest. That covers comprehensive medical care with no claim limits on major procedures. In India, private health insurance runs ₹15,000 to 50,000 annually for reasonable coverage, but serious illness or hospitalization can generate significant out-of-pocket costs depending on the plan. The German system is more expensive on paper but more comprehensive in practice.

Tax: What You Actually Take Home

A €60,000 gross salary in Germany results in roughly €38,000 to 40,000 in hand after Tax Class I deductions and social contributions. The breakdown for a single professional: income tax at 14 to 42% on a progressive scale, health insurance at about 7.3% employee share, pension at 9.3%, unemployment at 1.3%, and care insurance at about 1.7%. Total deductions are typically 35 to 42% of gross, leaving 58 to 65% as net.

India’s take-home is higher as a percentage. A ₹25 lakh gross salary under the new tax regime typically results in ₹19 to 20 lakhs net, a take-home rate of 76 to 80%. EPF contributions of 12% of basic salary are also partially employer-funded and build into a retirement corpus, so the deduction is less punitive than German social contributions.

| Component | India (₹25 lakhs gross) | Germany (€60,000 gross) |

|---|---|---|

| Gross Annual Salary | ₹25,00,000 | €60,000 |

| Income Tax | ₹3,50,000 (14%) | €12,000 (20%) |

| Social Contributions | ₹1,20,000 (EPF 12%) | €10,500 (17.5%) |

| Total Deductions | ₹4,70,000 (19%) | €22,500 (37.5%) |

| Net Annual Salary | ₹20,30,000 | €37,500 |

| Net Monthly Salary | ₹1,69,167 | €3,125 |

| Take-Home Percentage | 81% | 62.5% |

Note: Calculations are approximate and assume single tax filer, Tax Class I in Germany. Actual deductions vary based on individual circumstances, state, and specific benefits. German figures include health insurance, pension, unemployment, and care insurance.

For PPP comparison purposes, it’s worth running the calculation on net salary rather than gross. A €60,000 German gross becomes €37,500 net. Apply PPP: €37,500 × (20.421988 ÷ 0.700862) = approximately ₹10.9 lakhs in Indian purchasing power. Your ₹25 lakh Indian gross becomes ₹20.3 lakhs net, which is almost double the net purchasing power of that German salary after taxes.

The German Benefits That PPP Doesn’t Capture

The PPP calculator compares salary to salary. It doesn’t capture what German employment includes beyond pay.

Unemployment insurance (Arbeitslosenversicherung) pays up to 60% of your last net salary for 12 months if you lose your job, provided you’ve worked in Germany for at least 12 months. For someone relocating to a new country without a financial safety net, this matters. India has no equivalent protection for salaried professionals.

Pension contributions during your German working years build into a state retirement benefit. The system is funded and structured, unlike India’s EPF which is largely self-managed. If you work in Germany for several years, you accumulate pension entitlements that pay out in retirement.

Parental leave pays 65% of net salary for up to 14 months shared between both parents (Elterngeld). For anyone planning a family in their 30s, this is a significant benefit that doesn’t appear in any salary comparison. In India, maternity leave is mandated at 26 weeks with full pay for the mother, but paternity leave is typically two weeks and often not enforced.

None of this changes the PPP calculation. It means a €60,000 German package with full benefits competes differently with a ₹28 lakh Indian package than the raw numbers suggest. Factor it in when the decision is genuinely close.

Visa: What German Offers Qualify

The EU Blue Card is the main route for Indian professionals. For 2026, the standard salary threshold is €48,300 gross annually. For shortage occupations including IT, engineering, and most STEM roles, the threshold drops to €43,760. Most professional offers qualify.

The Skilled Worker Visa is the alternative, requiring a recognized qualification and a specific job offer. German recognition of Indian degrees varies by field. Engineering and IT qualifications from reputable Indian institutions generally qualify. Degrees from universities not on the recognition list may require an assessment, which adds time.

A less-known provision: IT professionals with at least two years of relevant work experience can qualify for the EU Blue Card without a formal degree. Germany recognizes practical skills in technology shortage areas.

Processing time for German work visas from India currently runs 8 to 12 weeks. Appointment slots at German consulates in India have been constrained, so apply as early as possible once you have a formal offer.

Work Culture: Hours and Leave

German employment law sets the standard work week at 40 hours with a statutory maximum of 48 hours including overtime. Overtime must be compensated in time off or pay. Most professional roles stay at 40 hours. Vacation entitlement is a minimum of 20 days annually by law, with most professional contracts providing 25 to 30 days plus public holidays.

Indian tech and finance roles frequently run 45 to 55 hours per week, with startups and high-growth companies expecting more. Vacation is typically 12 to 20 days depending on the company, and taking full leave is often culturally discouraged at some organizations.

If you’re evaluating a German offer against an Indian one at similar purchasing power, the additional 5 to 8 hours of free time per week and 5 to 10 extra vacation days per year have real value that doesn’t appear in any salary figure.

When Does Germany Make Financial Sense?

The Germany move makes direct financial sense when the offer clears your PPP equivalent by a meaningful margin. Enter your Indian salary in the PPP calculator with Germany as the target. Treat anything below that figure as a lateral move. A 20 to 30% buffer above it represents a genuine purchasing power improvement that covers relocation costs and the adjustment period.

Early and mid-career professionals with 3 to 10 years of experience tend to get the most from a German stint even when the first role doesn’t improve purchasing power. European credentials, DACH-region company names on a CV, and the breadth of international project exposure often compound into significantly higher earnings over five to ten years. The short-term purchasing power reduction is a career investment with a measurable long-term return for the right person in the right role.

Senior professionals at ₹40 lakhs and above often have more purchasing power staying in India, particularly in Bengaluru, Hyderabad, or Mumbai tech and finance roles. The PPP equivalent of ₹40 lakhs is roughly €1,37,000 in Germany. Realistic senior German offers rarely reach that. Add property, family, and an established professional network and the case for staying is strong.

The clearest financial winner is a remote role paying global rates while you live in India. You capture the income level without the cost of living.

How to Use the Calculator for a Job Decision

Enter your current Indian salary in the PPP calculator with Germany as the target country. The number you get is your purchasing power baseline in euros. Any German offer below that means your standard of living gets worse, regardless of how the number looks on screen.

Then adjust for net salary. A €70,000 gross German offer becomes roughly €43,000 to €45,000 in hand after Tax Class I deductions. Run the PPP calculation on that net figure, not the gross, for an accurate comparison.

Budget separately for relocation. The deposit on a German apartment is typically three months rent upfront plus the first month, so plan for €4,000 to €6,000 just to move in. Add visa fees, flights, and the gap between your last Indian paycheck and your first German one and you’re looking at ₹4 to 7 lakhs in total upfront cost before your German income starts.

For a step-by-step walkthrough of the calculator, see the how to use PPP calculator guide.

PPP Calculator India vs Germany: FAQ

Our calculator uses official World Bank PPP conversion factors, the same data international economists use. It provides accurate purchasing power comparisons based on standardized price levels. However, individual spending patterns may vary, and some expenses like housing can differ significantly even within the same country.

Use net salary for the most accurate comparison. Tax rates differ dramatically between India and Germany, affecting take-home pay significantly. Calculate net salary first, then apply PPP conversion to understand real purchasing power. Our calculator works with gross figures but explains that net salary provides better insight.

The calculator focuses on purchasing power of salary. German benefits like comprehensive healthcare, pension contributions, and unemployment insurance add value beyond raw salary numbers. Factor these benefits separately when evaluating total compensation. They typically represent 15-20% additional value.

Sometimes yes. If the role is a significant career step, if the company has a strong promotion track, or if the German experience unlocks higher-paying roles later, the short-term purchasing power reduction can be worth it. Run the five-year scenario, not just year one.

The World Bank calculates PPP at the country level, so the calculator gives you a single Germany figure. In practice, Munich costs noticeably more than Berlin or Leipzig, particularly for rent. If you are comparing offers from different German cities, add roughly 15 to 20% to your Munich baseline relative to Berlin. Frankfurt falls between the two.

Jitender is the founder and lead developer of PPPCalculator.info. He created this free tool to bridge the gap between currency conversion and real purchasing power, helping professionals across 50+ countries make informed salary decisions. He regularly translates complex World Bank and OECD data into practical guides for remote workers and expats.