Exchange rates convert currencies. PPP compares what those currencies actually buy. That distinction matters every time you evaluate a job offer abroad, negotiate a remote salary, or decide whether relocating makes financial sense.

In late 2021, the Turkish lira lost nearly half its value against the US dollar in a matter of weeks. A software engineer in Istanbul watched their salary shrink dramatically in dollar terms, almost overnight. But their rent didn’t double. Their groceries didn’t suddenly cost twice as much. Their daily life barely changed.

The currency market said one thing. The grocery store said something completely different. That gap is the difference between exchange rates and purchasing power parity, and understanding it changes how you read every international salary number.

Understanding PPP vs exchange rates changes how you evaluate international opportunities, negotiate remote salaries, and plan relocations.

Exchange Rates Track Currency Markets, Not Your Grocery Bill

An exchange rate is a price. It tells you how much one currency costs in terms of another. When you see “1 USD = 90 INR,” that number reflects what currency markets have decided the rupee is worth relative to the dollar at that moment.

That price moves constantly. It reacts to interest rate decisions, political events, trade patterns, and investor confidence. The Japanese yen weakened dramatically against the dollar between 2022 and 2024, mostly because the Bank of Japan kept interest rates near zero while the US Federal Reserve raised them aggressively. Nothing about the cost of ramen in Tokyo changed during that period.

The yen lost value because money was flowing out of Japanese bonds and into American ones, not because Japanese goods got cheaper.

This is the core limitation. Exchange rates are set in financial markets by people trading currencies for profit or managing risk. The rate between the dollar and the pound has almost nothing to do with what a loaf of bread costs in London versus Chicago.

When exchange rates are the right tool: sending money between countries, converting investment returns, pricing imports and exports, budgeting for a two-week vacation. In all of these situations, the bank rate is what you’ll actually pay or receive.

PPP Compares What Money Actually Buys

PPP measures what your money can purchase in everyday life, not what it converts to on currency markets.

The World Bank’s International Comparison Program tracks prices for roughly 3,000 goods and services across 176 countries. Bread, rent, bus tickets, medical visits, electricity, haircuts. From all those prices, the World Bank works out a single number for each country, called a conversion factor, that captures how far a dollar’s worth of spending actually goes there.

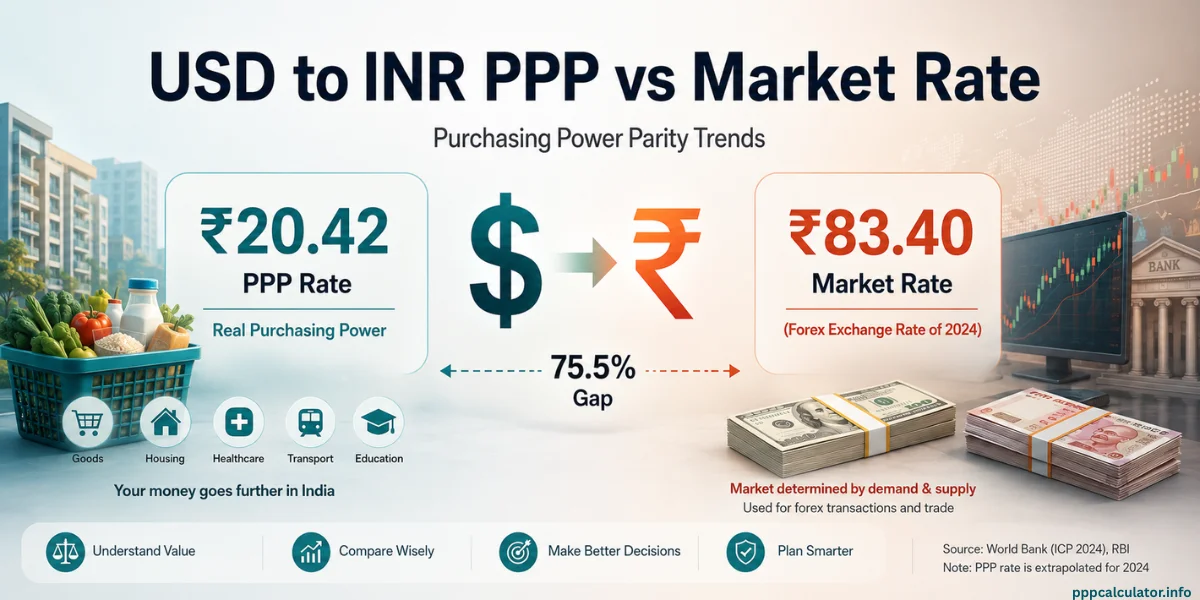

India’s conversion factor is 20.20. That means goods costing $1 in the US cost about 20.20 rupees in India. The exchange rate says $1 equals roughly 90 rupees. That gap between 20.20 and 90 is the whole story: a rupee buys far more inside India than the currency market gives it credit for.

For a deeper dive into how these factors are calculated and where they come from, see the purchasing power parity formula guide on this site.

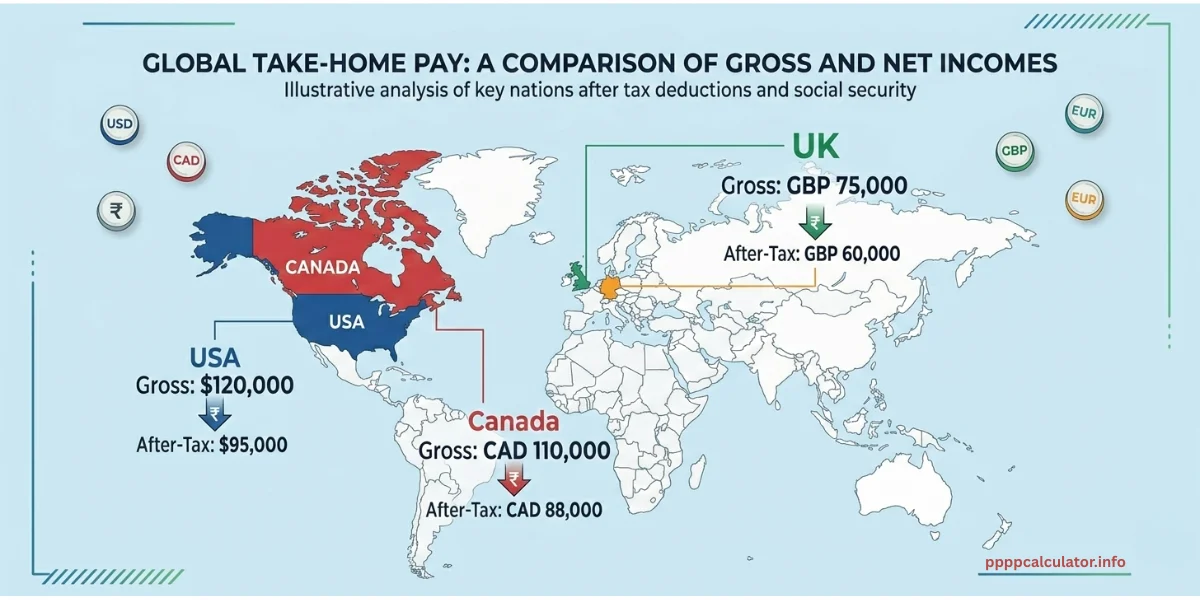

PPP vs Exchange Rate: Salary Comparison Across 7 Countries

The table below shows how the same salaries look through each lens. Exchange rate figures use approximate market rates. PPP figures use World Bank 2023 conversion factors.

| Country | Local Salary | Exchange Rate (USD) | PPP Equivalent (USD) |

|---|---|---|---|

| USA | $100,000 | $100,000 | $100,000 |

| India | ₹25,00,000 | $29,762 | $123,747 |

| UK | £55,000 | $69,850 | $80,538 |

| France | €45,000 | $48,600 | $63,329 |

| Germany | €55,000 | $59,400 | $75,539 |

| Canada | C$90,000 | $65,700 | $79,134 |

| Japan | ¥8,000,000 | $53,333 | $84,125 |

Japan’s ¥8 million looks like $53,333 but buys $84,125. Even within Europe, the same euro amount stretches differently in France versus Germany because local prices aren’t identical. The India vs USA comparison guide digs deeper into the biggest gap in this table.

The Economist’s Big Mac Index captures this idea in a single product: the same burger costs $5.69 in the US and roughly $3.25 worth of euros in Germany. Same ingredients, different price, because local costs differ. PPP applies that logic across thousands of goods instead of just one.

You can run these comparisons for your own salary and country pair using the PPP calculator with verified World Bank data for 196 countries.

How PPP vs Exchange Rate Affects Real Job Offers

Using the wrong method can make you reject a good offer or accept a bad one.

Say you’re earning $95,000 in Chicago and a Tokyo role comes in at ¥9,500,000. As per prevailing exchange rate, ¥9,500,000 = $60,000. Looks like a 37% pay cut, so your gut says no. But in purchasing power terms, that Tokyo salary buys about $99,900 worth of life. The offer actually matches your Chicago lifestyle almost exactly, and Japan’s national health insurance would cost you a fraction of what you’re paying in the US. The exchange rate made a perfectly good offer look terrible.

It works the other way too, and this version is sneakier because it feels good instead of bad. A Zurich offer that looks like a massive raise after currency conversion can quietly disappoint you once you’re there. Switzerland is one of the most expensive countries on earth. That “huge raise” in purchasing power terms might be a lateral move, or even a step down once you factor in Zurich rent and mandatory health insurance.

Whether it’s still worth it depends on things PPP can’t tell you, the career you’d build, whether you’d stay long enough for the Swiss pension to matter, what it does for your resume. The exchange rate said “easy yes.” The real answer is “it depends.”

These decisions get even trickier when someone considers moving back to their home country. A couple in Toronto earning C$150,000 might dismiss a Bangalore offer of ₹30 lakhs because the exchange rate makes it look like barely $21,000. In purchasing power, it funds a completely different lifestyle. The India vs Canada comparison guide breaks down why that corridor surprises so many people.

Why PPP and Exchange Rates Give Different Numbers

If exchange rates and PPP measured the same thing, they’d produce the same number. They don’t, and the gap between them is large and persistent. The honest answer for why is that several forces push them apart, and nobody fully agrees on which one matters most in a given situation.

Services can’t be shipped. This is the single biggest reason. A haircut, a dental cleaning, a month of rent, a taxi ride. These things are produced and consumed locally, so their prices reflect local wages and local demand, not global currency markets. A haircut costs $50 in Zurich and $3 in Hanoi because Swiss barbers earn Swiss wages. The exchange rate between the franc and the dong captures none of this.

There’s actually a name for this pattern, the Balassa-Samuelson effect. countries with lower wages systematically have cheaper services, which means their currencies look “undervalued” by exchange rates but perfectly valued by PPP. India’s rupee isn’t weak because Indian goods are bad. It’s cheap on currency markets because Indian wages are lower, which makes Indian services dramatically cheaper than their American equivalents.

Currency markets react to money flows, not prices. Exchange rates move when investors shift money between countries chasing better returns, when governments step in to strengthen or weaken their currency, and when traders bet on political outcomes. None of this has anything to do with what bread costs. Exchange rates overreact to headlines. PPP barely moves.

Limitations of PPP as a Salary Comparison Tool

PPP has real limitations, and pretending otherwise would make this article no different from the dozens that treat PPP as a perfect measure.

The biggest blind spot is spending patterns. PPP assumes you spend money like the average local person. If your budget tilts heavily toward internationally priced goods (iPhones, designer clothing, imported wine, international flights) PPP will overstate how far your money stretches in a lower-cost country. A ₹25 lakh salary buys a lot of local goods in India, but an iPhone 16 costs roughly the same everywhere in the world once you include taxes.

The What is Purchasing Power Parity guide on this site covers these spending pattern blind spots in more depth.

PPP is a national average. It tells you nothing about city-level differences. Living in Mumbai on ₹25 lakhs and living in a Tier-2 city on the same salary are vastly different experiences, but PPP treats them as identical. Same story in Japan, where ¥8 million in central Tokyo and ¥8 million in Fukuoka buy completely different lifestyles, but the PPP factor doesn’t care.

Your money may also stretch further in a country with weaker healthcare, fewer career options, or different safety standards. PPP captures none of that. It’s a purchasing power number, not a quality-of-life number.

When to Use PPP vs Exchange Rate

This part is actually simple once you stop overthinking it.

Use the exchange rate when actual currency conversion is involved. Sending money home to family. Buying something priced in a foreign currency. Selling overseas investments and bringing the money back. Budgeting for a short trip abroad. In all these cases, the exchange rate is the number you’ll actually transact at.

Use PPP when you’re comparing what life costs in two different places. Evaluating a job offer in another country. Negotiating a remote work salary. Deciding whether relocating makes financial sense. Setting international compensation as an HR team. For all of those, the exchange rate is basically useless because it ignores local prices entirely.

The most common mistake is mixing the two. People convert their salary using the exchange rate but then estimate their future expenses using PPP logic, or the reverse. Pick the method that matches your question and stick with it.

The step-by-step guide to using a PPP calculator walks through exactly how to apply PPP correctly for salary decisions.

Combining PPP, Exchange Rate and After-Tax Pay

Here’s the thing nobody tells you, neither method alone gives you a complete answer. The smartest move is to use both, plus a third layer that most salary comparison articles completely ignore: after-tax take-home pay.

Start with the PPP-adjusted salary to understand purchasing power. Then check the actual exchange rate to understand what happens when you send money home or buy internationally priced goods. Then run the salary through a tax calculator like SalaryAfterTax.com to see what you’ll actually deposit each month.

Take a Canadian offer of C$90,000. The exchange rate, PPP, and after-tax calculation each tell you a different number, and each one matters for a different part of your financial life. PPP tells you what that salary buys in everyday Canadian life.

The exchange rate tells you what it’s worth if you send money abroad. The tax calculator tells you what actually hits your bank account. The PPP calculator handles the purchasing power layer. SalaryAfterTax handles the tax layer. Together, they answer the question that neither tool answers alone.

Once you get how PPP and exchange rates work differently, international salary numbers stop being confusing and start being useful. The PPP Concepts hub covers the full framework if you want to go deeper.

PPP Vs Exchange Rate – FAQ

Not necessarily. For developed country pairs like the US and UK, the gap is small and stable. For pairs like the US and India, it has persisted for decades because the wage differential that makes Indian services cheap changes very slowly. Currency crises can widen the gap fast, and it can take years to settle back.

Both. The exchange rate determines how many rupees hit your bank account. PPP determines what those rupees buy. You benefit from the exchange rate on the way in and from PPP on the way out, which is exactly why earning in a strong currency while living in a lower-cost country works so well financially.

Because they’re optimizing for different things. Some pay a flat global rate using exchange rates. Others adjust for equivalent lifestyle using PPP. A third group blends market salary data with PPP bands. The approach often varies even within the same company depending on the role.

For short trips, exchange rates are more practical because you’re converting money and spending at market prices. PPP helps you choose where to go. If your dollar has twice the purchasing power in Portugal compared to Switzerland, your travel budget stretches further in Lisbon than Zurich.

Jitender is the founder and lead developer of PPPCalculator.info. He created this free tool to bridge the gap between currency conversion and real purchasing power, helping professionals across 50+ countries make informed salary decisions. He regularly translates complex World Bank and OECD data into practical guides for remote workers and expats.