What Indian Salaries Are Worth Abroad (PPP-Adjusted)

| Country | Foreign Salary | Equivalent Purchasing Power in India |

|---|---|---|

| Singapore | SGD 120,000 | ₹30.2 lakhs |

| Japan | ¥10,000,000 | ₹21.2 lakhs |

| Qatar | QAR 360,000 | ₹32.1 lakhs |

| Saudi Arabia | SAR 360,000 | ₹36.9 lakhs |

| Switzerland | CHF 120,000 | ₹24.2 lakhs |

| South Korea | ₩60,000,000 | ₹14.5 lakhs |

| Ireland | €70,000 | ₹18.3 lakhs |

All figures calculated using World Bank PPP conversion factors

Not every Indian professional considering a move abroad is looking at the US, UK, Canada, or Australia. In fact, some of the most common relocation corridors for Indian workers lead to places that rarely get their own salary comparison guides.

Singapore hires thousands of Indian tech professionals every year. Japan is actively recruiting Indian engineers to fill gaps left by its shrinking workforce. The Gulf states, specifically Qatar, Saudi Arabia, and Kuwait, employ millions of Indians across engineering, healthcare, finance, and construction. And then there are the European destinations that keep popping up in offer letters: Ireland, the Netherlands, Switzerland, Poland.

Each of these countries has a PPP factor wildly different from India’s. That means the gap between what a salary looks like at the exchange rate and what it actually buys varies enormously. It all depends on where you are headed.

PPP Calculator India vs Other Countries guide is not a surface-level list. It breaks down the purchasing power parity comparison for every major India corridor that does not already have a dedicated guide on this site. If you are comparing offers from the USA, UK, Canada, Germany, Australia, or Dubai, those posts go deeper on each corridor. This one covers everything else.

Key Takeaways

- Every corridor between India and another country has its own financial personality. Tax-free Gulf salaries behave completely differently from high-tax European packages.

- Asian tech hubs like Singapore and Japan each come with hidden costs that PPP alone does not capture.

- Before comparing any international offer to your current Indian salary, you need the PPP-adjusted number as your starting point, not the exchange rate number.

- The PPP calculator gives you that starting point in seconds. From there, the real work begins. You need to understand what each country adds or subtracts from that baseline through taxes, benefits, housing costs, and long-term financial structures.

How PPP Works Across Different Countries

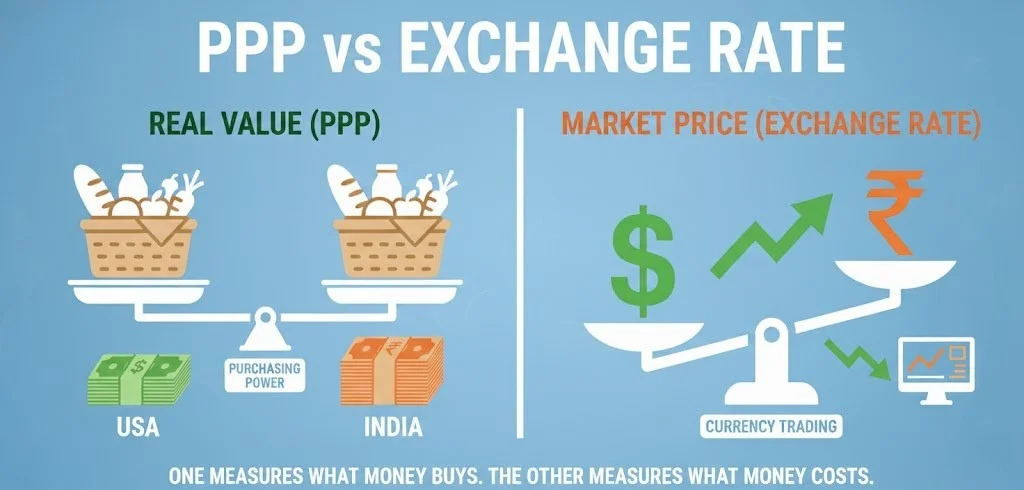

Most people comparing salaries across countries convert the number using the exchange rate and call it a day. That gives you a number in rupees, but it tells you nothing about what that money actually buys.

PPP uses a different approach. It compares the price of a common basket of goods and services, things like groceries, rent, transport, and healthcare, between two countries. The result tells you how much purchasing power a salary carries, not just how many rupees it translates to.

Here is a practical example. A software engineer in Singapore earning SGD 120,000 might convert that to roughly ₹75 lakhs using the exchange rate. Impressive on paper. But the PPP calculator tells a different story: that SGD 120,000 has the same purchasing power as about ₹30.2 lakhs in India. The exchange rate makes Singapore salaries look three times larger than what they actually feel like. Once you are paying Singapore rent, grocery bills, and transport costs, that illusion fades fast.

This pattern shows up everywhere, but the size of the gap differs dramatically by country. And that is exactly what makes a multi-country comparison so useful.

PPP Calculator: India vs Singapore

Singapore is the most expensive country in this entire guide when you measure the gap between exchange rate conversion and PPP reality.

To have the same purchasing power as SGD 80,000 in Singapore, you would need about ₹20.1 lakhs in India. At SGD 120,000, the equivalent drops to ₹30.2 lakhs. Even at SGD 200,000, which is a senior director-level salary, the PPP equivalent is ₹50.3 lakhs in India.

Going the other direction, an Indian salary of ₹25 lakhs carries the same purchasing power as roughly SGD 99,500 in Singapore.

What PPP Misses About Singapore

Singapore’s headline tax rate is low, topping out at 22% for income above SGD 320,000. For most Indian professionals earning SGD 80,000 to SGD 150,000, the effective tax rate falls between 5% and 11%. That is significantly lower than India’s tax burden at equivalent earning levels.

But Singapore takes its pound of flesh through housing. Renting a one-bedroom apartment in the city center runs SGD 2,500 to SGD 4,000 per month. A two-bedroom condo suitable for a family can easily hit SGD 4,500 to SGD 6,500. After 2022, rental prices jumped sharply and have not come back down.

There is also the CPF (Central Provident Fund) to consider. If you are a Singapore permanent resident, your employer contributes up to 17% and you contribute 20% of your salary into this fund. That is money locked away for housing, healthcare, and retirement. It builds wealth long-term, but it reduces your monthly cash flow significantly.

For Indians on an Employment Pass (no PR), CPF does not apply. Your take-home is higher, but you also have no safety net. Healthcare comes out of pocket unless your employer provides insurance.

The practical takeaway: Singapore offers high absolute salaries, favorable taxes, and a strong professional ecosystem. But the cost of daily life, especially housing and childcare, eats into that advantage more aggressively than most people expect.

PPP Calculator: India vs Japan

Japan is an interesting case because the PPP numbers make it look like a poor deal, but the full financial picture is more balanced than it first appears.

To have the same purchasing power as ¥6,000,000 (a common starting salary for mid-career professionals) in Japan, you would need about ₹12.7 lakhs in India. A salary of ¥10,000,000, which is strong for a senior engineer or manager, has the purchasing power of roughly ₹21.2 lakhs in India. At ¥15,000,000, the equivalent is ₹31.9 lakhs.

What Makes Japan Different

Japan’s PPP factor (95.10) is high relative to India’s (20.20), which means prices in Japan are substantially higher than in India when measured in local currency terms. But Japan also has systems that offset this in ways PPP does not account for.

Company housing subsidies are common. Many Japanese employers either provide company apartments at heavily discounted rates or pay a portion of your rent directly. For an Indian engineer joining a mid-size or large Japanese company, this benefit alone can reduce your effective housing cost by 30% to 50%.

Healthcare in Japan is universal and affordable. The national health insurance system covers 70% of medical costs, and your share of the premium is income-based. For a family, this represents massive savings compared to paying for private health insurance in Singapore or out-of-pocket healthcare costs in the Gulf.

Transport allowances are standard. Almost every Japanese employer covers your commuting costs fully, which might not sound like much until you realize that monthly train passes in Tokyo can run ¥15,000 to ¥30,000.

The tax burden is real, though. Effective income tax plus residence tax for someone earning ¥10,000,000 sits around 25% to 30%. Add social insurance premiums (pension, health, employment insurance) at roughly 15% of salary, and your take-home shrinks noticeably.

Japan also has a major non-financial factor: the language barrier. Career growth for Indian professionals who do not speak Japanese tends to plateau after a few years, unless you are in a multinational working primarily in English. The financial picture might work on paper, but career trajectory should weigh into the equation.

PPP Calculator: India vs Gulf Countries

The Gulf corridor (Qatar, Saudi Arabia, Kuwait) works on fundamentally different math than anywhere else in this guide, because of one factor: zero income tax.

Qatar: To have the same purchasing power as QAR 180,000 (a mid-level professional salary) in Qatar, you would need about ₹16.1 lakhs in India. At QAR 360,000, the equivalent is ₹32.1 lakhs. At QAR 600,000, it is ₹53.5 lakhs.

Saudi Arabia: SAR 180,000 in Saudi Arabia carries the same purchasing power as about ₹18.5 lakhs in India. At SAR 360,000, the equivalent is ₹36.9 lakhs.

Kuwait: KWD 15,000 per year in Kuwait has the same purchasing power as roughly ₹15.1 lakhs in India. At KWD 24,000, the equivalent is ₹24.1 lakhs.

The Tax-Free Advantage and Its Limits

None of these three countries charge personal income tax. Every riyal, every dinar you earn is yours to keep. For an Indian professional paying 20% to 30% in Indian income tax, this is a massive shift.

But PPP calculations do not factor in tax. When the calculator tells you that QAR 360,000 has the purchasing power of ₹32.1 lakhs in India, it is comparing pre-tax purchasing power. In reality, your ₹32.1 lakh equivalent in India would be reduced by income tax, while your QAR 360,000 stays intact. The tax-free advantage effectively inflates your real purchasing power beyond what PPP shows.

This is why many Indian professionals working in the Gulf report higher savings rates than their PPP-equivalent counterparts in India, even though the cost of goods is higher.

Where the Gulf Takes It Back

The Gulf’s financial story is not as simple as “no tax equals more money.” Several factors erode the advantage.

Housing costs vary wildly. In Doha and Riyadh, renting a two-bedroom apartment in a decent area runs QAR 6,000 to QAR 10,000 or SAR 4,000 to SAR 8,000 per month. Some employers provide housing allowances or company accommodation. If yours does not, housing can consume 30% to 40% of your salary.

Schooling is the other major expense. International school fees in Doha start at QAR 20,000 per year for primary school and climb to QAR 50,000 or more for senior levels. In Riyadh, comparable schools charge SAR 15,000 to SAR 50,000 annually. For families with two children, this becomes a significant line item.

There is also the employment structure to consider. Gulf work visas are tied to your employer through the sponsorship (kafala) system. While reforms have loosened restrictions in recent years, especially in Qatar and Saudi Arabia, changing jobs is still not as straightforward as it is in India or Singapore.

Long-term financial planning looks different too. The Gulf countries do not offer the kind of pension systems you find in Japan, Europe, or even India’s EPF. Your retirement savings are entirely self-directed. End-of-service gratuity provides a lump sum when you leave, typically calculated as 15 to 21 days of basic salary per year of service, but that is not a pension.

When the Gulf Corridor Makes Sense

The Gulf works best financially when three conditions align: your employer covers housing (or provides a generous housing allowance), you do not have children in expensive international schools, and you are disciplined about saving and remitting money home. Under those conditions, the combination of tax-free income and moderate living costs creates a savings rate that is hard to match anywhere else.

The India vs Dubai PPP guide covers the UAE-specific version of this math in more detail.

PPP Calculator: India vs European Destinations

Several European countries show up regularly in offer letters for Indian professionals but do not get the dedicated attention of the UK or Germany corridors. Here is a quick PPP look at the most common ones.

Ireland

Ireland has become a major tech hub, hosting European headquarters for Google, Meta, Apple, and dozens of smaller firms. A salary of €70,000 in Ireland has the same purchasing power as about ₹18.3 lakhs in India (using Ireland’s PPP factor of 0.771239).

The catch is Ireland’s tax system. Between income tax, USC (Universal Social Charge), and PRSI (social insurance), someone earning €70,000 takes home roughly €48,000 to €50,000. Dublin housing costs are notoriously high, with one-bedroom apartments in the city center running €1,800 to €2,400 per month.

On the positive side, Ireland’s healthcare system (a mix of public and private) and its position as an English-speaking EU country make it attractive for long-term settlement. The path to citizenship through naturalization takes about five years.

Switzerland

Switzerland is the outlier in every salary comparison. CHF 120,000 sounds extraordinary until PPP tells you it has the purchasing power of about ₹24.2 lakhs in India. Switzerland’s PPP factor (1.001601) is almost identical to the US baseline of 1.00. Prices in Switzerland are roughly on par with the US, but the strong Swiss franc makes exchange rate conversions wildly inflate how the salary looks in rupees.

Income tax in Switzerland varies by canton (state) and can range from 20% to 40% total. Health insurance is mandatory and expensive, running CHF 300 to CHF 500 per month per adult. But salaries are structured to account for these costs, and Swiss employers often contribute to pension funds that build significant wealth over time.

Netherlands

A salary of €65,000 in the Netherlands has the purchasing power of roughly ₹17.2 lakhs in India. The Netherlands offers the 30% ruling for highly skilled migrants. This tax benefit makes 30% of your salary tax-free for up to five years. That ruling significantly improves the real financial picture beyond what PPP alone shows.

Housing in Amsterdam is expensive and competitive, but cities like Eindhoven, Rotterdam, and Utrecht offer more reasonable alternatives.

Poland

Poland is emerging as a surprise destination for Indian tech workers, largely thanks to companies opening development centers in Warsaw, Krakow, and Wroclaw. A salary of PLN 180,000 carries the purchasing power of about ₹18.2 lakhs in India. Poland’s cost of living is substantially lower than Western Europe, which means your PLN goes further on rent, groceries, and dining out than the PPP number suggests for day-to-day essentials.

The trade-off is lower absolute salary levels compared to Ireland or the Netherlands.

PPP Calculator: India vs Asian Neighbors

South Korea

South Korea’s ₩60,000,000 salary (a solid mid-career figure) has the same purchasing power as roughly ₹14.5 lakhs in India. Seoul is expensive, but Korean companies typically offer benefits that shift the picture: housing deposits (jeonse system support), meal allowances, and performance bonuses that can add 15% to 30% on top of base salary. The language barrier is significant for career progression outside of multinational firms.

Malaysia

Malaysia is one of the most affordable destinations for Indian professionals. MYR 96,000 per year has the same purchasing power as about ₹13.6 lakhs in India. The cost of living in Kuala Lumpur is considerably lower than Singapore, and Malaysia’s cultural familiarity for Indians (large Indian diaspora, similar food, Hindu temples throughout the country) makes the adjustment smoother. Tax rates are moderate, topping out at 30% for income above MYR 2,000,000.

Thailand

Thailand appears on this list because of growing remote work and startup opportunities. THB 1,200,000 (about THB 100,000 per month) has the purchasing power of roughly ₹22.8 lakhs in India. Bangkok offers a high quality of life at costs well below Singapore or Tokyo. However, formal employment visas for Indians in Thailand can be complex, and the income tax system charges 5% to 35% on a progressive scale.

Why PPP Is Your Starting Point, Not Your Final Answer

Every number in this article comes from the same formula: multiply the foreign salary by the ratio of India’s PPP factor to the target country’s PPP factor, using World Bank conversion data. The PPP calculator on this site does this math for you instantly for any country pair.

But PPP measures average purchasing power across a standard basket of goods. Your personal spending pattern will always differ from the average. If you spend heavily on housing (Singapore, Dublin, Zurich), PPP understates how expensive your life actually is. If you are a single professional eating cheaply and living in shared accommodation (Gulf, Japan with company housing), PPP overstates the cost.

Taxes are the biggest variable PPP ignores. The difference between earning QAR 360,000 tax-free in Qatar and €65,000 at a 40% effective rate in the Netherlands is enormous. This remains true even if their PPP equivalents in India look similar.

The most reliable approach is to use PPP as your baseline comparison, then layer on the country-specific factors covered in this guide: tax rates, housing norms, employer benefits, healthcare costs, and long-term financial structures like pensions or provident funds.

For deeper dives into specific corridors, the PPP Comparisons hub has dedicated guides for India vs the US, UK, Canada, Germany, Australia, and Dubai.

Conclusion

Comparing salaries across a dozen countries sounds overwhelming, but the logic is always the same. Start with the PPP-adjusted number to strip away the illusion created by exchange rates. Then look at taxes, housing, employer benefits, and the specific costs that matter to your life stage.

The corridors in this guide cover a wide range of financial realities, from the tax-free Gulf to high-cost Singapore to affordable Malaysia. None of them is universally “better” or “worse.” Each one rewards a different kind of professional situation.

Run your specific numbers through the PPP calculator, use this guide to understand what PPP does not capture, and you will have a clearer picture than 90% of people making international career decisions.

For more on how purchasing power parity works and dedicated country guides, explore the resources across this site.

Frequently Asked Questions

There is no single “best” country because it depends on your industry, tax situation, and spending habits. Gulf countries like Qatar and Saudi Arabia offer the strongest savings potential because of zero income tax, but only if your employer covers housing. Singapore and Switzerland offer the highest absolute salaries, but their high cost of living significantly reduces purchasing power.

PPP is more useful for understanding what a salary actually buys in daily life. The exchange rate tells you how many rupees you would get if you converted the foreign currency today. PPP tells you whether those rupees would buy a similar lifestyle. For anyone evaluating a job offer or planning a move, PPP gives a more realistic picture than the exchange rate.

Often yes, but not always. A QAR 360,000 salary in Qatar (PPP equivalent ₹32.1 lakhs) is entirely take-home. A €70,000 salary in Ireland (PPP equivalent ₹18.3 lakhs) is reduced by roughly 30% after taxes. However, European salaries come with benefits like public healthcare, pension contributions, and long-term residency rights that the Gulf does not match.

The PPP calculator on this site supports all 196 countries with World Bank PPP data. Select your source country (India) and the target country, enter your salary, and the tool converts it instantly. The result shows what that salary is worth in purchasing power terms. For context on what the number means for your specific situation, this guide covers the most common corridors.

Because the cost structures are fundamentally different. Singapore concentrates its high costs in housing and childcare. Japan spreads costs more evenly but adds high taxes and social insurance. The Gulf keeps taxes at zero but charges heavily for housing and schooling if your employer does not cover them. PPP gives you the average comparison, but your actual experience depends on which cost categories hit your personal budget hardest.

Jitender is the founder and lead developer of PPPCalculator.info, with a background in software development and international economics. He created this free tool to bridge the gap between currency conversion and real purchasing power, helping professionals across 50+ countries make informed salary decisions. He regularly translates complex World Bank and OECD data into practical guides for remote workers and expats.