A £50,000 salary in London sounds like ₹55 lakhs at today’s exchange rate. For someone earning ₹15 lakhs in Bangalore, that sounds life-changing.

But the exchange rate hides something important: close to 40% of that £50,000 never reaches your wallet. Income tax, National Insurance, council tax, and the immigration health surcharge all take their share first. On top of that, everyday expenses like groceries, rent, and transport cost two to three times more than back home.

The purchasing power parity between India and the UK paints a much more realistic picture than the exchange rate ever could. Getting this right can mean the difference between a smart career move and a financial shock.

Use PPP calculator India vs UK above to compare your specific salary. The numbers below break down what the results actually mean for your daily life.

Key Takeaways

- A £50,000 UK salary has the same purchasing power as roughly ₹14.8 lakhs in India, not the ₹55 lakhs the exchange rate shows.

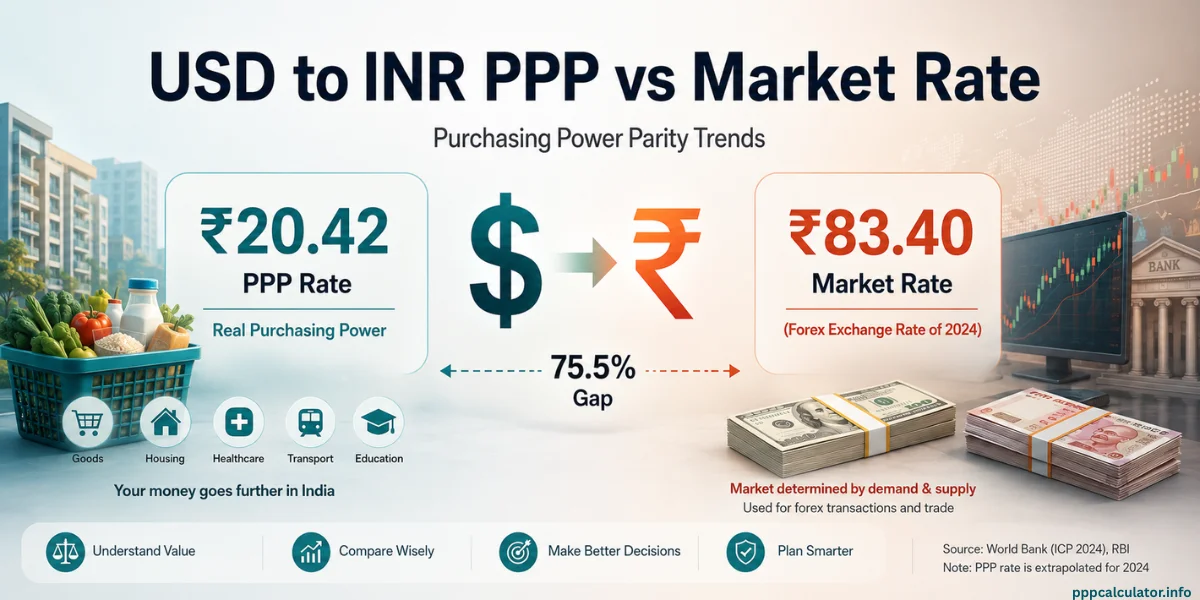

- The UK’s PPP factor is 0.683 and India’s is 20.20, so one pound of buying power in the UK equals about ₹29.58 of buying power in India.

- UK income tax and National Insurance together take 30-40% of a mid-range salary before you see any of it.

- Free NHS healthcare is a major financial benefit that PPP numbers alone cannot capture, especially compared to India’s high out-of-pocket medical costs.

- London pays 30-50% more than the rest of the UK, but PPP uses national averages, so the real gap is even wider outside London.

Quick Reference: India vs UK PPP Salary Equivalents

| UK Salary (£) | India Equivalent (₹) | India Equivalent (Lakhs) |

|---|---|---|

| £30,000 | ₹8,87,490 | ≈ ₹8.9 lakhs |

| £50,000 | ₹14,79,150 | ≈ ₹14.8 lakhs |

| £80,000 | ₹23,66,640 | ≈ ₹23.7 lakhs |

| India Salary (₹) | UK Equivalent (£) |

|---|---|

| ₹10 lakhs | £33,803 |

| ₹20 lakhs | £67,606 |

| ₹35 lakhs | £1,18,311 |

What PPP India vs UK Actually Tells You

When you run the PPP calculator India vs UK, the result can feel surprising. A salary that looks three or four times bigger in pounds often buys a similar lifestyle to what you already have in India.

PPP works like a lifestyle translator rather than a currency converter. The World Bank measures what everyday things like food, housing, and transport actually cost in each country. The UK’s PPP factor of 0.683 means a pound stretches slightly further than a dollar. India’s factor of 20.20 means a rupee goes much further at home than its exchange rate would suggest.

So when you earn £50,000 in London, the PPP equivalent in India is about ₹14.8 lakhs. This does not mean your salary converts to ₹14.8 lakhs. It means the flat you rent, the meals you cook, and the bus you ride in London on £50,000 add up to roughly the same standard of living that ₹14.8 lakhs would give you in India.

That changes the question you should ask before moving, Instead of “How much more will I earn?”, the better question is “What kind of life will this salary give me?”

How UK Taxes Shrink Your Salary Before You Spend It

Purchasing Power Parity compares what things cost in two countries. It does not account for how much of your pay you actually keep. In the UK, the gap between your salary on paper and the money in your bank account is one of the widest among developed countries. Our PPP formula guide walks through the calculation method, but taxes are the part the formula leaves out.

What Gets Deducted from Your UK Pay

In the 2025/26 tax year, UK income tax works in bands. The first £12,570 you earn is tax-free (your personal allowance). You pay 20% on anything from £12,571 to £50,270, 40% on earnings from £50,271 to £125,140, and 45% above that. National Insurance adds another 8% on earnings between £12,571 and £50,270, dropping to 2% on anything higher.

There is also a trap that catches many Indian professionals off guard.

If you earn over £100,000, your personal allowance shrinks by £1 for every £2 above that mark. By £125,140, the personal allowance disappears completely. That creates an effective tax rate of about 60% on everything you earn between £100,000 and £125,140.

How This Plays Out on a £50,000 Salary

On £50,000, you pay about £7,486 in income tax and roughly £2,994 in National Insurance. Then add council tax, which runs £1,200 to £2,500 a year depending on where you live. Your actual take-home lands around £37,000 to £38,000, about 74-76% of your gross.

Now compare that with India. The PPP equivalent of £50,000 is ₹14.8 lakhs. Under India’s new tax regime, the effective tax on ₹14.8 lakhs is considerably lower. So even though PPP says these two salaries are “equal” in buying power, the Indian salary leaves more money in your hands after taxes.

The New India-UK Free Trade Agreement

India and the UK wrapped up a Free Trade Agreement in May 2025 that includes something especially useful for Indian workers: social security coordination. Until now, Indian professionals on temporary UK assignments paid National Insurance they could never claim back once they returned home.

The new deal aims to fix this. If you are on a short-term posting of up to three years, you could save a meaningful chunk of your salary. For temporary moves, this changes the financial picture quite a bit.

Where Your Pounds Go: Real UK Costs for Indian Expats

PPP relies on national averages. But your spending happens in a specific city, in a specific neighbourhood. The UK has one of the biggest regional cost gaps in Europe, and your location changes everything about how far your salary stretches.

Why London Is a Different Country

London salaries in sectors like finance, tech, and professional services run 30-50% above the national average. That sounds great until you see the rent. A one-bedroom flat in central London (Zones 1-2) goes for £1,500 to £2,200 a month. The same flat in Manchester, Birmingham, or Edinburgh costs £700 to £1,100.

The PPP factor of 0.683 covers the whole UK. So if you are moving to London, your real purchasing power is lower than what PPP suggests. If you are heading to a northern city, it is higher. This is exactly why a city-level PPP calculator would be valuable but does not yet exist at the World Bank level.

Costs That Surprise Indian Expats

Some UK expenses have no real equivalent in India, and they add up quietly.

Council tax is something every UK household pays. It goes toward waste collection, road repairs, and local policing. Expect £100 to £250 per month depending on your property and area. There is nothing quite like this in India.

A TV licence costs £169.50 a year if you watch live television or use BBC iPlayer. It is a legal requirement, not optional.

Transport eats into your budget fast. A monthly London Tube pass for Zones 1-3 runs about £170. Annual rail season tickets for commuters outside London can cost £3,000 to £5,000. Compare that to Indian metros, auto-rickshaws, and ride-hailing services that stay dramatically cheaper.

Childcare is possibly the biggest shock. Full-time nursery for one child in London costs £1,200 to £1,800 a month. That single expense can swallow over a quarter of a mid-range take-home salary. In India, between family support and affordable help at home, this cost barely shows up.

NHS Healthcare: A Big Benefit PPP Cannot Measure

One of the most important financial advantages of living in the UK is something the PPP formula completely overlooks: the National Health Service. The NHS gives all legal residents free access to GP visits, hospital treatment, emergency care, maternity services, and most specialist referrals.

As an Indian professional on a Skilled Worker visa, you pay an Immigration Health Surcharge (IHS) when you apply. This runs about £1,035 per year. Once paid, your NHS access is the same as any British citizen.

Think about what that replaces. In India, out-of-pocket healthcare costs make up a huge share of total medical spending. A serious hospital stay at a good private hospital can easily cost ₹2-5 lakhs, even with insurance. In the UK, the same treatment costs nothing beyond the IHS you already paid.

For a family of four, the IHS totals roughly £4,140 per year. A comparable family health insurance plan at a reputable Indian private hospital might cost ₹50,000 to ₹1.5 lakhs annually, and you still face co-pays, waiting periods, and exclusions. The NHS eliminates all of that.

The trade-off is speed. Non-urgent NHS referrals can take weeks or months. About 13% of UK residents buy supplemental private insurance for quicker specialist appointments, which adds £1,000 to £2,000 a year to your costs.

UK Pensions: The Retirement Benefit Hidden in Your Salary

Most PPP comparisons skip this entirely, but workplace pensions add real value to UK compensation packages and change the long-term math of an India vs UK salary comparison.

Every UK employer must auto-enrol you in a workplace pension scheme. The minimum total contribution is 8% of qualifying earnings, split as at least 3% from your employer and 5% from you. Many employers in finance and tech contribute 6-10% or even more. This is extra money on top of your salary that PPP calculations never show.

On a £50,000 salary with a 6% employer contribution, that is £3,000 per year invested toward your retirement. Over a 10-year UK career, this compounds into a sizeable pension pot, especially with the tax relief you get on your own contributions.

The tricky part comes when you leave the UK. Your pension stays in a UK scheme, and transferring it to India through a Qualifying Recognised Overseas Pension Scheme (QROPS) involves limited options and complicated tax rules. If you return to India, this money also sits in pounds, exposed to whatever the GBP-INR exchange rate does over the years.

India’s EPF currently offers guaranteed returns around 8.25%, well above what most UK pension funds deliver. If the salary comparison between India and the UK is already close, the pension maths on each side could tip your decision.

When Does Moving to the UK Make Financial Sense?

On pure purchasing power, the numbers often favour staying in India. But careers are about more than purchasing power. Here are the situations where a UK move pays off in ways PPP cannot capture.

Career Growth and Global Exposure

In industries like finance, consulting, law, and academic research, UK experience acts as a career accelerator. Two to three years working in London can open doors to senior roles in India or elsewhere that might take much longer to reach otherwise. The long-term salary boost from that career jump often outweighs the purchasing power gap during your UK years.

The Savings and Remittance Advantage

Indian professionals who live lean in the UK can take advantage of a useful gap between PPP and exchange rates. You earn and budget in pounds at PPP rates, but you save and send money home at exchange rates. Someone saving £1,000 a month in the UK can remit roughly ₹1.1 lakhs to India at current rates, far more buying power than saving the same effort from an Indian salary would produce.

Purchasing Power Parity measures what money buys where you live. The exchange rate measures what your savings buy when they cross borders. If building savings to bring home is part of your plan, the exchange rate works in your favour on that portion.

Professional Credentials That Travel

UK qualifications like ACCA, CIMA, RICS, or hands-on experience with UK regulatory and business frameworks carry significant weight in India’s job market. Professionals returning from the UK often see salary jumps of 30-50% compared to peers who stayed. Our salary comparison by country guide shows how different countries stack up for building portable career value.

How the UK Compares to the US for Indian Professionals

If you have offers from both countries on the table, the PPP dynamics between the two corridors are quite different. The India vs US purchasing power parity comparison shows that $100,000 in the US equals roughly ₹20.2 lakhs in buying power. US salaries tend to be higher, taxes lower in many states, and housing more affordable outside major metros. But the US has no NHS-style safety net, health insurance is expensive, and employment protections are weaker.

The UK offers lower gross pay and higher taxes, but wraps in benefits that the US does not mandate: free NHS healthcare, 28 days minimum paid leave, and automatic workplace pension enrolment. Your total compensation package in the UK is broader than the headline salary suggests.

The choice comes down to what matters more to you: higher cash in hand and savings potential (US), or stability, social protections, and a healthcare safety net (UK). If you are also considering Continental Europe, our India vs Germany comparison covers a similarly benefit-heavy model.

Making Your Decision

Purchasing power parity between India and the UK gives you a starting point, not a final answer. A £50,000 UK salary works out to just ₹14.8 lakhs in PPP terms, but it also comes with NHS healthcare, employer pension contributions, paid leave, and a professional network that spans the globe.

What makes sense for you depends on where you are in your career, what you are optimising for, and how long you plan to stay. A three-year sprint to build credentials and save aggressively looks very different from a permanent move to settle with family.

Plug your own numbers into our purchasing power parity calculator, then add in the tax, healthcare, pension, and career factors covered in this article. The right answer is always personal, but with the right data, you do not have to rely on guesswork.

PPP Calculator India vs UK – FAQ

Ans: The UK’s PPP factor is 0.682911 and India’s is 20.202558, both based on 2023 World Bank data. Dividing India’s factor by the UK’s gives you a ratio of about 29.58, which means one pound of purchasing power in the UK is roughly equal to ₹29.58 of purchasing power in India.

Ans: No, PPP only compares prices of goods and services between two countries. It does not account for taxes, deductions, or take-home pay. Since UK income tax and National Insurance can take 25-40% of a mid-range salary, you need to calculate your net pay separately before comparing lifestyles.

Ans: It depends on where you live. After tax and National Insurance, £40,000 leaves you with about £31,000-£32,000 a year. Outside London, that supports a comfortable lifestyle for a single person. In London, it covers the basics but leaves little room for savings, especially once rent takes its share.

Ans: The FTA includes a social security agreement that lets Indian professionals on temporary UK postings (up to three years) avoid paying National Insurance contributions they could never claim back. This can save roughly 8-13% of qualifying earnings, making short-term UK assignments significantly more affordable than before.

Ans: It depends on what you are trying to figure out. PPP shows you what lifestyle a salary supports in each country, so it is better for comparing quality of life. The exchange rate tells you what your savings are actually worth when you send money home. Most people need both: PPP to evaluate the job offer, and the exchange rate to plan their savings and remittances.

Jitender is the founder and lead developer of PPPCalculator.info. He created this free tool to bridge the gap between currency conversion and real purchasing power, helping professionals across 50+ countries make informed salary decisions. He regularly translates complex World Bank and OECD data into practical guides for remote workers and expats.