A senior developer in Bangalore earning ₹25 lakhs gets an offer from a Sydney firm for AUD 120,000. He runs the exchange rate math, sees ₹64 lakhs, and assumes his lifestyle will more than double. Eighteen months later, he is living in a shared apartment in Parramatta, watching his savings barely match what he put away back home.

His salary tripled on paper. His grocery bill, rent, and childcare tripled in reality. This story repeats across thousands of Indian professionals migrating to Australia every year. The missing piece is almost always the same: nobody told them about purchasing power parity before they signed.

Australia is a unique corridor for Indians because the financial picture has more moving parts than almost any other destination. Your employer quietly adds 12% of your salary into a retirement fund you may never fully access. Your healthcare costs flip dramatically the day you get permanent residency.

The same AUD 120,000 buys a comfortable family life in Adelaide but leaves you stretched thin in Sydney. None of this shows up in a simple salary conversion.

This article pairs the India vs Australia PPP results with the practical context you need to evaluate an Australia move properly, covering superannuation, Medicare, the city cost divide, visa pathway finances, and the factors that make this corridor genuinely different from US or Canada.

Key Takeaways

- Australia’s mandatory 12% superannuation adds real value on top of your salary that PPP calculations never capture, but temporary visa holders lose up to 65% of it in tax when they cash out after leaving.

- Living costs in Sydney can run 20-30% higher than in Perth or Adelaide for identical lifestyles, which means the same AUD salary delivers very different purchasing power depending on your city.

- Australia’s Medicare system covers most medical needs for permanent residents, but 482 visa holders must buy private health insurance (OVHC) out of pocket until they secure PR.

- The India-Australia corridor is unique because skilled migration offers a clear pathway to permanent residency, which changes how you should think about short-term salary versus long-term wealth building.

- PPP does not capture the “settlement cost cliff,” the AUD 15,000 to 25,000 you spend in your first three months on bond deposits, furniture, school enrollment, and car registration before your regular budget even kicks in.

Quick Reference: Salary Equivalents

| Australian Salary (AUD) | Indian Equivalent in Purchasing Power (INR) |

|---|---|

| AUD 60,000 | ₹8,85,302 (≈ ₹8.9 lakhs) |

| AUD 85,000 | ₹12,54,178 (≈ ₹12.5 lakhs) |

| AUD 120,000 | ₹17,70,605 (≈ ₹17.7 lakhs) |

| AUD 150,000 | ₹22,13,256 (≈ ₹22.1 lakhs) |

Calculated using World Bank PPP conversion factors

Why PPP Matters More Than the Exchange Rate

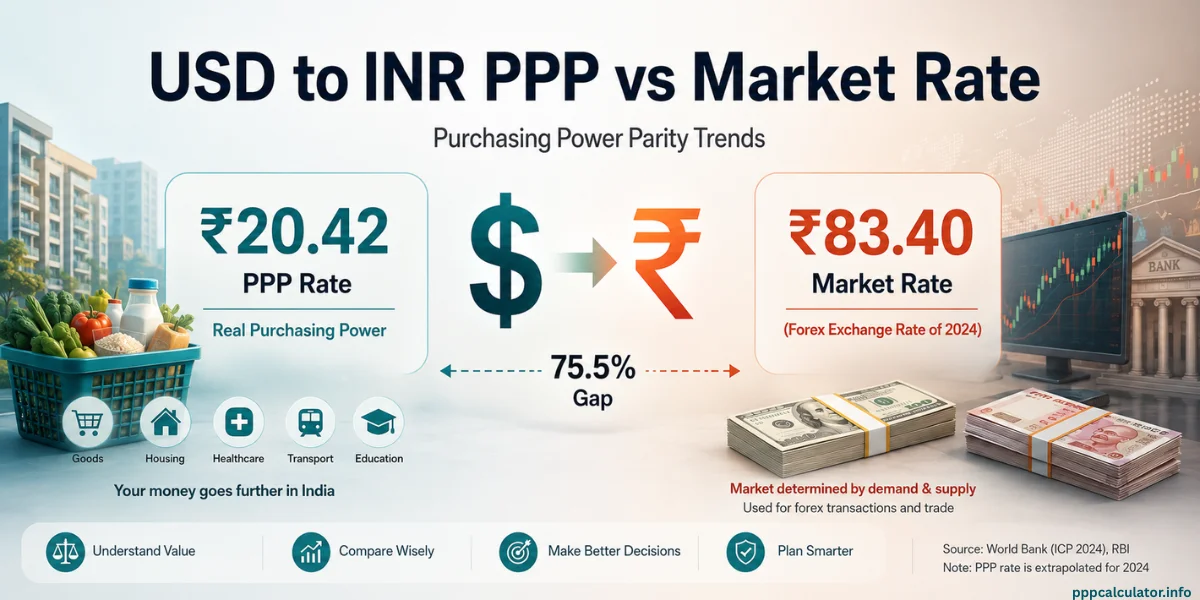

When you receive an Australian job offer, your first instinct is to multiply the salary by the AUD-INR exchange rate. At the time of writing, that rate hovers around ₹55-57 per Australian dollar. So AUD 120,000 looks like ₹76.50 lakhs. Impressive on paper.

But the exchange rate only tells you what your money converts to. It says nothing about what your money buys. A flat white coffee in Melbourne costs AUD 5.50. A comparable coffee in Bangalore costs ₹80-100. The exchange rate says the Melbourne coffee “costs” about ₹300, but PPP asks a different question: how much of your daily earning does that coffee consume?

That is why purchasing power parity exists. It compares what money actually buys in each country, using thousands of goods and services tracked by the World Bank’s International Comparison Program. Our calculator uses these official conversion factors to show you the real lifestyle a salary supports, not just the converted number.

The PPP conversion factor for India is 20.20 and for Australia it is 1.37. The ratio between them (about 14.76) tells you that AUD 1 in Australia has roughly the same buying power as ₹14.76 in India. Compare this to the exchange rate of ₹64 per AUD, and you can see the massive gap between what your salary converts to and what it actually buys.

Use the purchasing power parity calculator above to plug in your specific offer and see where you land.

The Superannuation Factor is Your Invisible Salary Boost

Here is where Australia stands apart from every other destination in country comparison guide. Every Australian employer must pay superannuation contributions on top of your base salary. As of July 2025, this rate is 12% of your ordinary earnings.

On an AUD 120,000 salary, your employer puts an additional AUD 14,400 into your super fund every year. This is not deducted from your pay. It is extra money, and it does not show up in any PPP calculation.

Over a five-year stint in Australia, that is AUD 72,000 in employer contributions alone, before investment returns. Add those returns (Australian super funds have averaged around 7-8% annually over the long term), and you are looking at a meaningful retirement asset.

The Catch for Temporary Visa Holders

If you are on a 482 visa (Skills in Demand visa) and you eventually leave Australia without getting permanent residency, you can claim your super back through the Departing Australia Superannuation Payment (DASP). But the tax hit is steep.

For non-working-holiday temporary residents, the ATO taxes the DASP at 35% on the taxed component and 45% on any untaxed portion. So that AUD 72,000 accumulated over five years could shrink to roughly AUD 47,000 after tax, before any fund exit fees.

This creates a fork in the road that every Indian professional in Australia faces. If you plan to get PR and stay long term, superannuation is a massive wealth-building advantage that PPP misses entirely. If you plan to return to India after a few years, a significant chunk of your super gets taxed away upon departure.

Your migration pathway shapes how you should weigh this benefit. And that is something no calculator, including ours, can factor in automatically.

The City Cost Divide: One Country, Many Price Tags

PPP conversion factors are national averages. They treat Australia as a single economy with one price level. Anyone who has compared rental listings in Sydney versus Adelaide knows that is far from reality.

Sydney: The Premium Price Tag

Sydney is Australia’s most expensive city by a comfortable margin. A two-bedroom apartment in the inner suburbs runs AUD 600-800 per week in rent. Childcare costs between AUD 120-180 per day. Groceries, petrol, and dining out all carry a Sydney surcharge.

For an Indian family arriving from, say, Hyderabad on an AUD 120,000 salary, Sydney’s costs can eat through that income fast. After tax, rent, childcare for one child, groceries, transport, and insurance, monthly savings may be thin, especially in the first year.

Melbourne: Slightly More Affordable, Still Expensive

Melbourne generally runs about 10-15% cheaper than Sydney for housing, though the gap narrows in trendy inner suburbs. It offers better public transport coverage, which can reduce car-related expenses. The coffee and food scene means cheaper eating options compared to Sydney, though “cheaper” is relative.

Perth, Brisbane, and Adelaide: Where PPP Stretches Further

These cities offer genuinely lower costs, particularly in housing. An AUD 120,000 salary in Perth or Adelaide delivers noticeably more purchasing power than the same salary in Sydney. Perth’s mining-adjacent economy also offers higher salaries in certain technical and engineering roles, creating a double advantage of higher pay and lower costs.

For Indian professionals with flexibility in where they land, choosing a city outside Sydney and Melbourne is one of the most powerful financial decisions you can make. The salary difference between cities is often small (AUD 5,000-15,000 for comparable roles), but the cost difference is enormous.

Beyond PPP: The Settlement Cost Cliff

One thing that catches almost every Indian migrant off guard is the upfront cost of setting up life in Australia. PPP compares ongoing living costs, the weekly groceries, the monthly rent, the annual insurance premium. It does not capture the one-time expenses that hit you in the first 90 days.

A realistic first-three-months budget for a family of four looks something like this:

- Four weeks of rental bond (AUD 2,400-3,200)

- furniture and household basics (AUD 3,000-6,000)

- A used car plus registration and insurance (AUD 8,000-15,000)

- School uniforms and enrollment fees (AUD 500-1,500 per child)

- Overseas Visitor Health Cover for the family (AUD 3,000-5,000 per year, paid upfront or quarterly)

- Various deposits for utilities and internet.

These first few months can easily consume AUD 15,000 to 25,000 beyond your normal living expenses. Indians moving from a fully established household in a city like Chennai or Bangalore often underestimate this because nothing equivalent exists when you are already settled at home.

Planning for this settlement cost cliff is essential. It sits entirely outside what PPP or any salary calculator can tell you.

Medicare and Healthcare: What Your Visa Decides

Australia’s public healthcare system, Medicare, is one of its strongest attractions. For permanent residents, it covers GP visits, public hospital treatment, specialist referrals, and subsidized prescriptions through the Pharmaceutical Benefits Scheme.

But your visa status determines your access. This creates a hidden cost divide that PPP cannot see.

On a 482 Visa (Temporary Skilled)

You do not qualify for Medicare. You must purchase Overseas Visitor Health Cover (OVHC), which typically costs AUD 3,000 to 5,000 per year for a family. OVHC covers hospital treatment and some extras, but it is not as comprehensive as Medicare. Out-of-pocket costs for specialists and dental are common.

After Getting PR

You gain full Medicare access. Your ongoing healthcare costs drop sharply. GP visits become free or heavily subsidized. Hospital treatment in the public system costs nothing. You still need private insurance if you want shorter wait times for elective procedures, but the financial safety net is dramatically stronger.

This transition from OVHC to Medicare is financially meaningful. For a family, it can save AUD 3,000 to 5,000 per year in insurance premiums alone, plus reduced out-of-pocket costs.

When you compare this to India, where good private health coverage for a family costs ₹50,000 to ₹1.5 lakhs annually but still comes with co-pays and exclusions, the post-PR healthcare advantage is substantial.

The Skilled Migration Angle: How PR Changes the Math

Australia’s skilled migration system directly affects how you should read PPP numbers. Unlike some other destinations where permanent residency is uncertain or distant, Australia offers structured pathways that Indian professionals regularly use.

The 482 visa (now called Skills in Demand visa) lets you work for up to four years. After working for the same employer for at least two to three years, you can apply for the 186 visa (Employer Nomination Scheme) for permanent residency.

The subclass 189 (Skilled Independent) visa offers another route based on a points system where age, English proficiency, work experience, and qualifications all count.

Why does this matter for PPP? Because the financial picture looks very different at year one versus year five.

In year one, you are on a temporary visa, paying for OVHC, unable to access certain government benefits, and your super is subject to departure tax if you leave. The PPP comparison at this stage underestimates your true costs.

By year three or four, with PR secured, you have Medicare, your super grows tax-efficiently, you can access the First Home Owner Grant, your children attend public school without international fees, and your long-term financial trajectory changes completely.

The PPP number stays the same. But the life it describes is fundamentally different depending on your residency status.

Running the Numbers in Reverse

The PPP calculator works in both directions. If you are an Indian professional considering whether to stay in India or move to Australia, here is what Indian salaries look like in Australian purchasing power terms.

| Indian Salary (INR per year) | Australian Equivalent in Purchasing Power (AUD) |

|---|---|

| ₹6,00,000 (₹6 lakhs) | AUD 40,664 |

| ₹10,00,000 (₹10 lakhs) | AUD 67,773 |

| ₹15,00,000 (₹15 lakhs) | AUD 1,01,660 |

| ₹25,00,000 (₹25 lakhs) | AUD 1,69,434 |

This table reveals something important. A ₹15 lakh salary in India delivers purchasing power equivalent to about AUD 101,660 in Australia. The median full-time salary in Australia is roughly AUD 70,000-75,000. So if you earn ₹15 lakhs in India, you would need an above-median Australian salary just to maintain the same lifestyle.

That does not mean the move is bad. It means you should negotiate with clear expectations. You can check what specific salaries are worth across borders using our salary comparison by country guide.

What PPP Gets Right and What It Misses

The PPP formula is powerful for comparing the everyday purchasing power of two salaries. It handles groceries, rent, transport, and basic services well because these items are part of the World Bank’s basket of goods.

But for the India-to-Australia corridor specifically, there are things PPP captures well and things it misses.

PPP captures well:

Housing costs, grocery prices, local transport, restaurant meals, utility bills, and general day-to-day expenses.

PPP misses:

Superannuation (12% employer contribution not reflected in salary), Medicare versus private insurance cost gap, settlement costs for new migrants, education costs that differ by visa status (international versus domestic school fees), remittance advantages (earning in AUD but sending home at favorable exchange rates), and the long-term wealth effect of permanent residency.

The smartest way to use the PPP calculator is as your starting point, not your final answer. Get the number, then layer on the factors from this article that apply to your situation.

Making Your Decision

Australia’s financial story has layers that sit above and below the PPP line. Above it: superannuation contributions, Medicare access after PR, the remittance advantage of earning in a strong currency. Below it: settlement costs, the city cost divide, visa-dependent expenses that shift dramatically once you secure permanent residency.

The most important variable is not the salary number. It is your time horizon. A three-year work stint with a return to India is a completely different financial calculation from a permanent migration. The first is a savings sprint where you optimize for exchange rate gains. The second is a wealth-building journey where superannuation, property, and Medicare compound in your favor over decades.

Plug your own numbers into the PPP calculator, then work through the factors in this article that apply to your personal situation. The right answer is always specific to you.

PPP Calculator India vs Australia – FAQ

Ans: The World Bank PPP conversion factor for India is 20.202558 and for Australia it is 1.36917. The ratio between them means that AUD 1 in Australia has roughly the same purchasing power as ₹14.76 in India. This is very different from the market exchange rate of roughly ₹64 per AUD, which is why PPP gives a more accurate picture of real salary value.

Ans: Yes. Temporary visa holders who leave Australia permanently can claim a Departing Australia Superannuation Payment (DASP) after their visa expires. However, the tax on this payout is 35% on the taxed component for non-working-holiday visa holders. You must apply through the ATO after leaving, and if you do not claim within six months, your super gets transferred to the ATO as unclaimed money.

Ans: In purchasing power terms, AUD 100,000 in Australia equals about ₹14.76 lakhs in India. Whether that is “good” depends heavily on your city. In Perth or Adelaide, a family of four can live comfortably and save on this salary. In Sydney, the same family would need to budget carefully, especially with children in childcare.

Ans: Australia’s PPP factor (1.369197) is higher than Canada’s (1.137311), which means the same salary amount goes slightly further in Canada than in Australia in purchasing power terms. However, Australia offers higher median salaries in many skilled occupations and mandatory 12% superannuation, which can offset this gap.

Ans: No. PPP compares what money buys, not how much you earn. Australian wages are significantly higher than Indian wages in absolute terms, which is why many Indians improve their overall financial position despite the lower purchasing power per dollar.

Jitender is the founder and lead developer of PPPCalculator.info. He created this free tool to bridge the gap between currency conversion and real purchasing power, helping professionals across 50+ countries make informed salary decisions. He regularly translates complex World Bank and OECD data into practical guides for remote workers and expats.